Why Gold Still Matters in a Fully Digital Economy: Tangible Value When Everything Else Is Bytes

In a world where finance is increasingly digital, with tokenized assets and central bank digital currencies, gold remains uniquely tangible. The reasons gold matters more, not less, as the rest of the financial system goes digital.

The financial world is becoming digital faster than at any time in history. Trading is electronic. Settlement is increasingly real-time. Assets are tokenized. Central bank digital currencies are being deployed across multiple major economies. Some critics argue that gold has become irrelevant in this digital era; an analog asset in a digital age. The argument is plausible but wrong. As more of the financial system becomes digital, the unique properties of physical gold become more, not less, valuable. Physical gold is the one major asset that cannot be hacked, frozen, deleted, or reprogrammed. In a fully digital economy, that property becomes the rarest and most important type of wealth.

Quick framing

Digital assets have many advantages: liquidity, traceability, integration with modern finance. Digital assets also have unique risks: cyberattacks, platform failures, regulatory freezes, programmable restrictions. Physical gold has none of these digital risks while sacrificing some of the digital advantages. The asymmetry makes gold more relevant, not less, in a digital economy.

The digital transformation of finance

- Electronic trading: stocks, bonds, commodities, FX all trade electronically.

- Real-time settlement: T+0 and T+1 settlement becoming standard.

- Tokenized assets: real estate, art, equity tokenization growing.

- Central bank digital currencies: China e-CNY, India e-rupee, EU digital euro projects.

- Bank deposit digitization: physical bank branches declining; mobile banking dominant.

- Cryptocurrency growth: Bitcoin, Ethereum, stablecoins reaching trillion-dollar valuations.

- Payment system evolution: real-time payments, programmable transactions, AI-driven routing.

What can go wrong in digital finance

1. Cyberattacks

Major financial cyberattacks have hit banks, exchanges, and payment systems repeatedly. The 2016 Bangladesh Bank heist stole 81 million dollars through the SWIFT system. The 2020 Twitter Bitcoin scam exploited account access. Multiple cryptocurrency exchange hacks have lost billions of dollars. In any digital system, sophisticated attackers can potentially compromise accounts, freeze positions, or steal value.

2. Platform failures

Even well-managed digital platforms experience outages. The 2024 CrowdStrike-Microsoft outage disrupted global financial systems for days. Multiple banking apps have experienced multi-day outages preventing customer access to funds. Exchange platforms occasionally halt trading during volatility, locking customers out at critical moments.

3. Regulatory freezes

Digital assets can be frozen by regulatory action far more easily than physical assets. The 2022 Canadian trucker convoy saw bank accounts frozen administratively without court order. The 2022 Russian sanctions froze 300 billion dollars of central bank reserves at financial institutions. Digital assets sit on systems that regulators can access; physical assets typically do not.

4. Programmable money restrictions

CBDCs and programmable digital currencies can in principle restrict specific purchases, expire after deadlines, or require positive identification for transactions. China's e-CNY already supports programmable money features. The technical capability exists; the political application will be determined by future policy decisions. Physical gold has no such restrictions.

5. Grid and connectivity failures

Digital assets require electricity and connectivity to access. Major power outages (Texas 2021, Spain Portugal 2025) have left people unable to access bank accounts, payment systems, or digital wallets for hours to days. In severe cyber or grid events, digital finance could be unavailable for longer periods. Physical gold continues to function without electricity or internet.

Why physical gold is structurally different

| Risk | Physical gold | Digital assets |

|---|---|---|

| Cyber attack | Immune | Vulnerable |

| Platform outage | Not applicable | Vulnerable for hours to days |

| Regulatory freeze | Possible but rare | Easy and instant |

| Programmable restrictions | Not applicable | Possible with CBDCs |

| Grid failure | Continues to function | Inoperable without power |

| Internet failure | Continues to function | Inoperable without network |

| Quantum computing threat | Immune | Vulnerable to future quantum |

| Counterparty failure | Not applicable | Significant risk |

| Bank holiday | Continues to function | Restricted access |

The CBDC challenge

Central bank digital currencies are being deployed or piloted by major economies including China, India, Brazil, Russia, and the European Union. The technical capability of CBDCs includes real-time transaction monitoring, programmable money (restrictions on what can be purchased), expiry dates, automated taxation, and identity-linked transactions. Even if specific CBDCs are deployed initially with minimal restrictions, the technical capability for restrictive features will exist. Physical gold remains the only widely-available form of wealth completely outside CBDC systems.

Why digital gold is not the same as physical

Tokenized gold (PAX Gold, Tether Gold, Kinesis) provides digital exposure to physical gold. The underlying gold is allocated at major custodians. This is useful for liquidity and integration with digital finance. But tokenized gold relies on the platform, the blockchain network, and the regulatory environment of the issuing entity. Tokenized gold is digital gold; it carries digital risks. Physical gold in hand has none of those risks. The two should be considered complementary, not interchangeable.

Quantum computing and digital money

Quantum computers are not yet cryptographically relevant, but they will be eventually (estimated 2035 to 2045). When they are, current encryption (RSA, elliptic curve) becomes vulnerable. Bitcoin, ETFs, and digital gold tokens all depend on this encryption. Physical gold has no cryptographic dependency and is unaffected by quantum computing. As Y2Q approaches, physical gold becomes the only widely-available asset immune to quantum-driven cryptographic disruption.

What digital advocates miss

- 1.Tangibility is a feature, not a bug: physical possession provides legal and practical certainty digital cannot match.

- 2.Disconnection from systems: not being part of any digital network is sometimes the strongest property.

- 3.5,000-year track record: gold has worked across every prior technology change.

- 4.Universal acceptance: gold trades globally without any digital infrastructure.

- 5.Cross-generational continuity: physical gold passes between generations without digital records.

- 6.Crisis resilience: gold functions through events that disable digital systems.

- 7.No system dependency: gold value does not depend on any system continuing to operate.

The complementary approach

The optimal approach in a digital economy is not gold versus digital, but gold and digital. Hold meaningful physical gold for the unique properties only physical can provide. Use digital tools (ETFs, tokenized gold, exchange-traded products) for liquidity and tactical exposure. Use traditional cash for short-term transactions. Use Bitcoin or other crypto for digital-native exposure. Each format serves different purposes; the combination provides resilience across more scenarios than any single asset can.

The next 20 years

- CBDC deployment accelerates: most major economies will have operational CBDCs by 2030.

- Asset tokenization expands: real estate, equity, and credit move to blockchain rails.

- Cyber risk grows: attack surface expands with digital integration.

- Programmable money increases: more financial products become smart contracts.

- Physical gold demand persists: emerging-market household demand continues.

- Central-bank gold accumulation continues: structural shift toward physical reserves.

- Quantum computing approaches relevance: cryptographic transition becomes urgent late in the decade.

- Gold's relative role grows: as digital wealth becomes more dominant, physical alternatives become more important.

Why central banks signal the answer

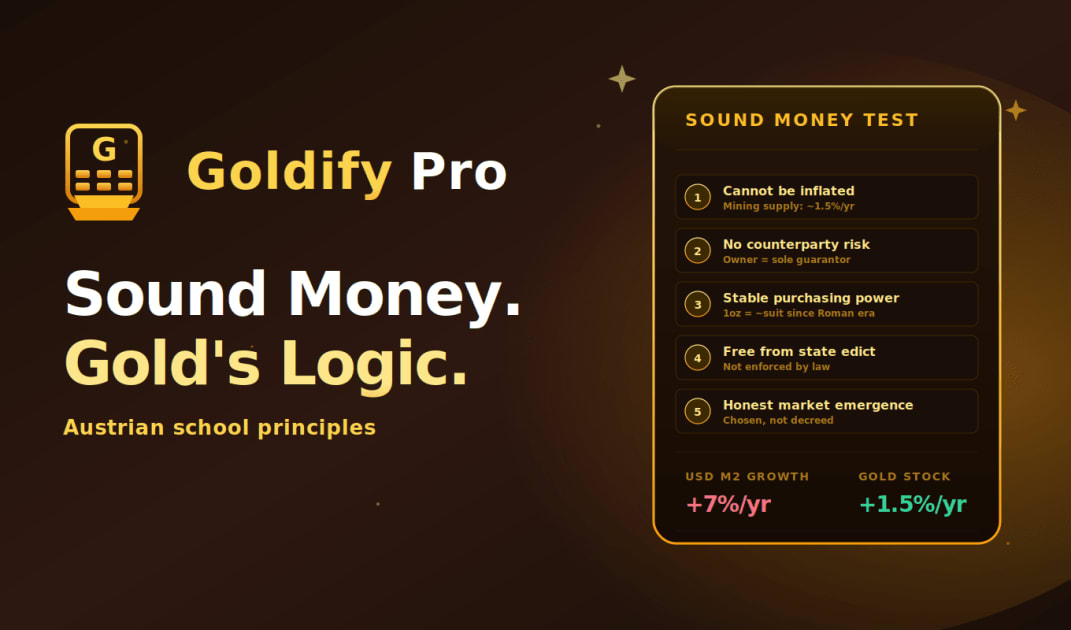

The institutions that should most embrace digital money (central banks themselves) are also accumulating physical gold at record rates. Net central-bank gold buying was over 1,000 tonnes per year in 2022, 2023, and 2024. Central banks understand digital money; they are building CBDCs. They are also building physical gold reserves. The implicit message is clear: digital money serves certain functions, physical gold serves others, and both are needed in a sophisticated reserve strategy. Private investors can draw the same conclusion.

Frequently asked questions

Does gold matter less now that finance is digital?

No, more. As more wealth becomes digital, the unique properties of physical gold (no counterparty, no system dependency, no cryptographic risk) become more valuable. Central banks accumulating gold at record rates demonstrate this institutional view.

Is digital gold a good substitute for physical?

Digital gold (PAX Gold, Tether Gold, gold ETFs) is useful for liquidity but carries digital risks that physical does not. The two are complementary, not interchangeable. Most serious gold investors hold both.

How will CBDCs affect gold?

CBDCs add to gold's relative value by demonstrating the contrast between programmable digital money and tangible physical wealth. The technical capability of CBDCs to restrict transactions or expire money makes physical gold uniquely outside that system.

Is gold immune to quantum computing?

Physical gold has no cryptographic dependency, so quantum computing cannot affect it. Digital gold tokens depend on current encryption and will need to migrate to post-quantum cryptography as quantum computers approach relevance.

Will physical gold become obsolete in a digital era?

Almost certainly not. The unique properties of physical gold (no counterparty, no system dependency, tangible possession) cannot be replicated by any digital form. As digital wealth becomes more dominant, physical alternatives become more important, not less.

What proportion should I hold in physical versus digital gold?

Depends on individual circumstances. A common approach: 30 to 50 percent in physical for crisis insurance, 50 to 70 percent in ETFs and digital instruments for liquidity. Adjust based on jurisdiction, total holdings, and personal risk tolerance.

Will gold prices rise in a digital economy?

The structural case supports it, though short-term moves are unpredictable. Central-bank buying continues, household demand in emerging economies grows, and digital risks add to gold's relative value. Long-term trajectory remains upward.

Disclaimer

Forecast and financial-advice disclaimer

Digital economy trends are evolving rapidly. Not investment advice. Consult licensed financial advisors for portfolio decisions in the context of digital and physical asset choices.

Editorial disclaimer

Digital economy data is drawn from named central bank, regulatory, and industry sources. Live gold rates appear on the Goldify Pro home page and live-gold-rates page.

Originality and AI policy

Researched and written by the Goldify editorial team. Every claim verified against named primary sources. We do not publish unedited AI output.

Tools mentioned in this article

Continue reading

Gold Education

Gold EducationWhy Gold Is Considered Anti-Government Money: Confiscation History, Capital Controls and Sovereign Independence

Gold Education

Gold EducationGold and Civilization: How Empires Used Gold to Gain Power from Rome to America

Gold Education

Gold Education