The Philosophy of Sound Money Explained Through Gold: Hard Currency, Mises, Rothbard and the Modern Debate

Sound money is currency that holds value across time without political intervention. Gold has been the historical standard. The philosophy traces from Aristotle to Mises to modern hard-money advocates. Why the debate matters today.

Sound money is currency that holds purchasing power across time without political intervention. The concept is centuries old and has been central to monetary debates from Aristotle through Adam Smith, Carl Menger, Ludwig von Mises, Friedrich Hayek, Murray Rothbard, and modern hard-money advocates. The 1971 abandonment of Bretton Woods made fiat money the global standard. The 2008 crisis and persistent post-2020 inflation have revived interest in sound money principles. Understanding the philosophy explains why some serious thinkers consider modern monetary policy fundamentally flawed.

Quick framing

Sound money: currency that maintains purchasing power without political manipulation. Historical examples: gold coinage from 600 BC to 1971, silver coinage similarly. Unsound money: currency easily inflated, debased, or politically controlled. Modern fiat: technically unsound by historical standards but accepted because no alternative is currently universal.

The historical intellectual lineage

Aristotle (384 to 322 BC)

Aristotle identified the six properties of money in his Politics and Nicomachean Ethics: durability, divisibility, portability, recognizability, scarcity, and consistent quality. He observed that gold and silver naturally satisfied these criteria and were therefore appropriate monetary substances. His framework remains the starting point for sound-money philosophy.

Adam Smith (1723 to 1790)

Smith's Wealth of Nations (1776) discussed money primarily as a facilitator of exchange. He recognized the dangers of currency debasement and supported the classical gold standard. Smith was less ideological than later Austrian thinkers but laid foundations for understanding monetary stability as essential to economic prosperity.

Carl Menger (1840 to 1921)

The founder of the Austrian school of economics. Menger's theory of money emerged from observing how some commodities became commonly accepted in barter exchange. He argued that money evolves spontaneously through markets rather than being created by government decree. Gold became money because it satisfied the most criteria for monetary use, not because any authority declared it so.

Ludwig von Mises (1881 to 1973)

The most influential 20th-century Austrian economist. His Theory of Money and Credit (1912) developed Menger's framework into a comprehensive theory of money. Mises argued that fiat currencies are inherently unstable because they enable governments to inflate, distort interest rates, and create boom-bust cycles. He advocated a return to commodity money (gold standard) as the most reliable monetary foundation.

Friedrich Hayek (1899 to 1992)

Nobel laureate and student of Mises. Hayek extended sound-money thinking and proposed currency competition (private currencies competing in the market) as an alternative to government monopoly. His Denationalisation of Money (1976) anticipated some modern cryptocurrency arguments. Hayek did not necessarily endorse gold specifically but advocated principles that historically have favored gold.

Murray Rothbard (1926 to 1995)

Rothbard popularized hard-money thinking for a broader audience. His America's Great Depression (1963) argued that the 1929 crisis was caused by Federal Reserve money creation in the 1920s. What Has Government Done to Our Money? (1963) explained gold-standard mechanics to general readers. Rothbard's framework remains influential in modern hard-money discussions.

Sound money criteria

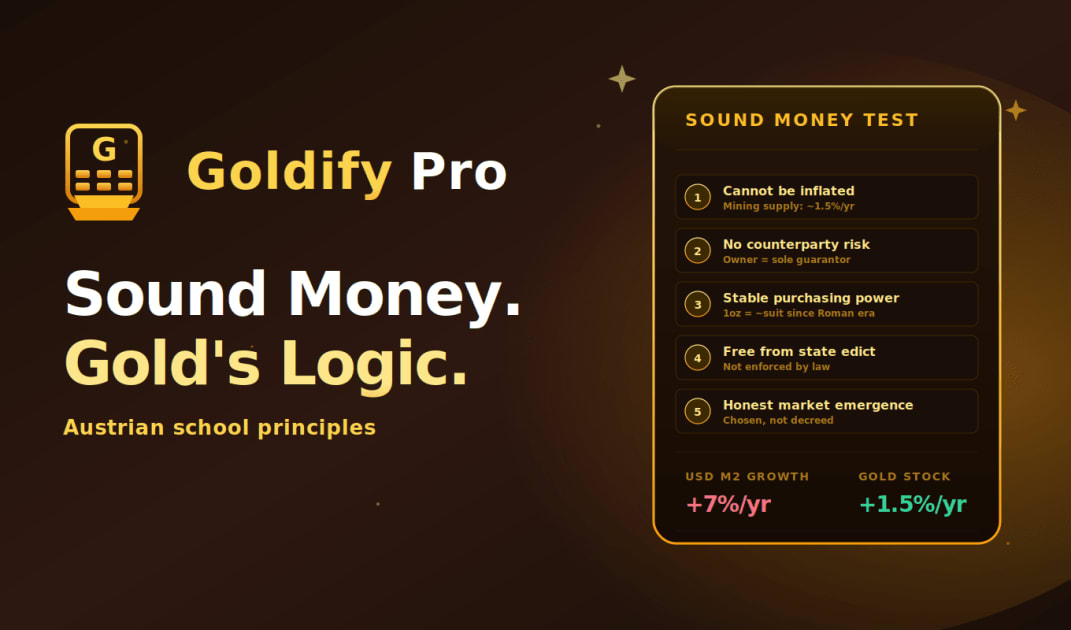

- 1.Stable supply growth: limited and predictable increase in monetary base.

- 2.Independent of political control: no government discretion over issuance.

- 3.Universally accepted: works across borders without official sanction.

- 4.Resistant to debasement: cannot be inflated by issuing authority.

- 5.Reliable across centuries: holds value over multi-generational horizons.

- 6.Convertible: can be exchanged for tangible assets at known rate.

- 7.Anti-cyclical: does not amplify business-cycle fluctuations through credit expansion.

The classical gold standard (1880 to 1914)

The classical gold standard is the closest historical approximation to pure sound money. Major economies fixed their currencies to specific weights of gold; international trade settled in gold flows; central banks held gold reserves against currency issuance. Inflation was negligible over the period. The system produced significant economic growth but also brutal recessions (1893, 1907) because monetary tightening could not be avoided through policy. World War I ended the system.

Why governments prefer fiat

- Fiscal flexibility: governments can fund deficits through monetary creation.

- Recession management: central banks can ease policy without gold reserves.

- War financing: rapid mobilization without taxing the public.

- Welfare state: large social programs require monetary policy flexibility.

- Banking system support: banks can be bailed out through liquidity creation.

- Political accountability: politicians prefer not to be constrained by gold.

- Inflation as stealth tax: real-value erosion of debt benefits debtors and governments.

Why hard-money advocates oppose fiat

- Hidden inflation tax: monetary debasement reduces purchasing power of savings.

- Boom-bust cycles: credit expansion creates artificial booms followed by busts.

- Wealth transfer: inflation benefits debtors (often government) at expense of savers.

- Mis-investment: artificially low interest rates create investments that fail when rates normalize.

- Moral hazard: bank bailouts incentivize excessive risk-taking.

- Political incentives: short-term election cycles favor monetary easing over discipline.

- Compounding effects: small annual debasement compounds to massive multi-decade losses.

The modern debate

Post-2008 monetary expansion and post-2020 stimulus have revived interest in sound-money principles. Critics point to persistent inflation, asset-price bubbles, growing wealth inequality, and fiscal unsustainability as evidence of fiat money's failures. Defenders point to economic growth, low official inflation for most of the past 40 years, and successful financial-crisis management as evidence of fiat money's successes. Both sides have valid points; the disagreement is partly about which timeframes and metrics matter most.

Bitcoin and digital sound money

Bitcoin advocates often invoke sound-money principles. Bitcoin has fixed supply (21 million coins), is independent of government, and is technically resistant to debasement. Critics counter that Bitcoin has not yet been crisis-tested across multiple generations and that its volatility limits its medium-of-exchange function. Whether Bitcoin becomes a permanent form of digital sound money remains an open question that the next 50 years will answer.

Does sound money work in practice?

The classical gold standard delivered low inflation and significant economic growth between 1880 and 1914. It also delivered painful deflations during recessions because monetary easing was constrained. The trade-off is real: sound money provides stability over decades at the cost of short-term economic management flexibility. Most modern governments have chosen flexibility over stability. Whether that choice was wise is itself a contested question.

What sound-money advocates actually want

- 1.A new gold standard: tying currencies to gold reserves with mandatory convertibility.

- 2.Sound-money sovereign wealth funds: government accumulating gold as long-term reserve.

- 3.Restored Fed gold restrictions: legal constraints on Fed balance sheet expansion.

- 4.Currency competition: allowing private gold-backed currencies alongside fiat.

- 5.Decentralized gold-backed digital money: blockchain-based gold token systems.

- 6.Gold revaluation: marking Treasury gold to market would create monetary tightening discipline.

- 7.Constitutional amendments: limiting government monetary discretion through fundamental law.

Where modern thinkers stand

- Mainstream economists: largely accept fiat money; advocate sensible policy.

- Modern hard-money advocates: Peter Schiff, Mike Maloney, James Rickards, Lyn Alden.

- Bitcoin advocates: Saifedean Ammous, Lyn Alden, Michael Saylor.

- Modern monetary theorists: defend fiat money as appropriate tool for sovereign government.

- Central bankers: support managed fiat money with inflation targeting.

- Some emerging-market governments: increasingly skeptical of US-dollar reserve system.

Frequently asked questions

What is sound money?

Currency that maintains purchasing power across time without political intervention. Historically, commodity-backed money (gold, silver) has been the most reliable form. Modern fiat money is technically unsound by these criteria but is the global standard.

Why does sound money matter?

Because the value of savings, retirement, and long-term contracts depends on how much purchasing power the currency retains over decades. Unsound money systematically erodes wealth held in cash and bonds.

Who was Ludwig von Mises?

The most influential 20th-century Austrian economist. His Theory of Money and Credit (1912) developed the framework that became modern hard-money philosophy. He advocated commodity money (gold standard) as more stable than fiat.

What is the Austrian school of economics?

An economic tradition emphasizing methodological individualism, subjective value theory, and market processes. Austrian economists generally favor commodity money over fiat, market interest rates over central-bank rates, and minimal government intervention.

Why is the gold standard not used today?

Because governments wanted monetary flexibility for fiscal financing, recession management, and welfare-state expansion. Fixed-weight gold convertibility constrained these objectives. The 1971 Nixon shock ended formal gold-dollar convertibility worldwide.

Could the world return to a gold standard?

Improbable in the short term but not impossible long-term. Partial gold backing (in BRICS settlement, in sovereign wealth funds) is being discussed. Full convertibility at fixed prices is unlikely but partial gold-anchored systems may emerge.

Is Bitcoin sound money?

It has properties of sound money (fixed supply, no central authority, resistant to debasement). It lacks the crisis-tested track record of gold. Whether Bitcoin becomes long-term sound money or remains a speculative asset is being determined now.

Disclaimer

Forecast and financial-advice disclaimer

Monetary policy debates are contested. Not investment advice. Readers should consult licensed advisors for portfolio decisions based on monetary theory.

Editorial disclaimer

Intellectual history is drawn from named academic sources, primary works by listed economists, and named monetary-history publications. Live gold rates appear on the Goldify Pro home page and live-gold-rates page.

Originality and AI policy

Researched and written by the Goldify editorial team. Philosophical analysis verified against named primary sources. We do not publish unedited AI output.

Tools mentioned in this article

Continue reading

Gold Education

Gold EducationWhy Gold Still Matters in a Fully Digital Economy: Tangible Value When Everything Else Is Bytes

Gold Education

Gold EducationWhy Gold Is Considered Anti-Government Money: Confiscation History, Capital Controls and Sovereign Independence

Gold Education

Gold Education