What Happens If Global Debt Crashes the Economy? Gold's Role When Sovereign Debt Becomes Unmanageable

Global debt has reached $315 trillion — over 333% of world GDP. What happens to your savings if a major sovereign defaults, central banks lose bond-market control, or a debt-deflation spiral takes hold? The historical playbook, the modern risks, and why gold has survived every prior debt crisis.

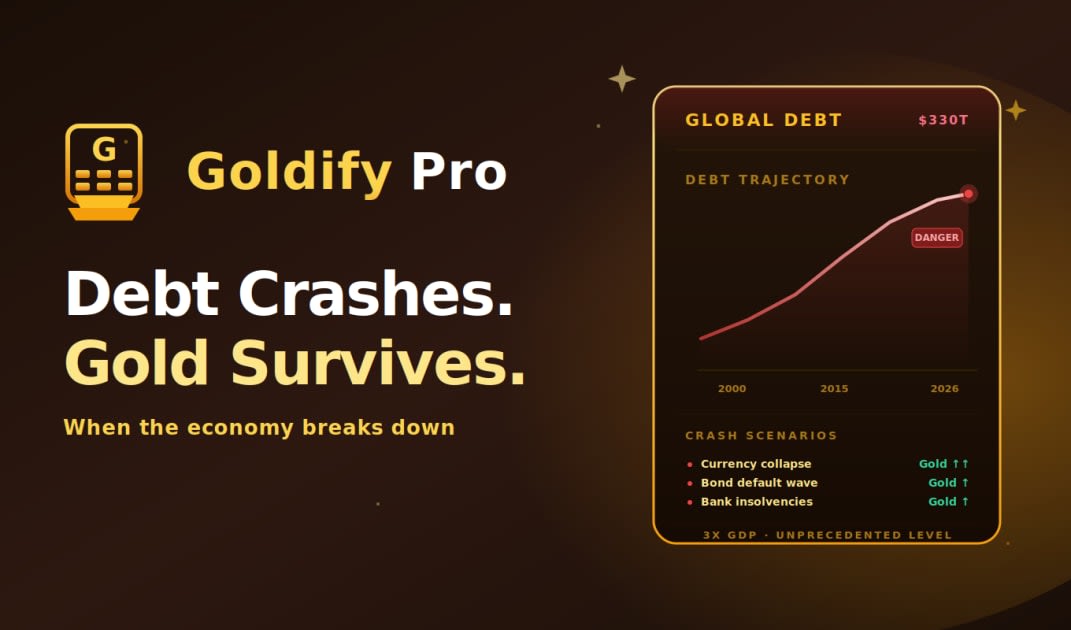

Total global debt has crossed $315 trillion — over 333% of world GDP, per the Institute of International Finance. That includes governments, households, financial firms and non-financial corporations. The number is the highest in recorded history, both in absolute terms and as a share of GDP. The question is no longer whether the debt is large; it is whether it is manageable — and what happens if it stops being.

Quick answer

A global debt crash would unfold in three phases: bond-market dislocation, currency devaluation, and inflation or deflation depending on policy response. Historically, gold has outperformed in all three phases — it is the only asset class with no issuer, no counterparty and no political dependency.

The numbers: how big the debt actually is

| Sector | Total debt | % of global GDP |

|---|---|---|

| Governments | ~$92 trillion | ~98% |

| Non-financial corporates | ~$94 trillion | ~99% |

| Financial sector | ~$72 trillion | ~76% |

| Households | ~$60 trillion | ~63% |

| Total | ~$315 trillion | ~333% |

Country-level debt-to-GDP

| Country | Debt-to-GDP | Trend (5y) |

|---|---|---|

| Japan | ~265% | Stable high |

| Italy | ~138% | Rising |

| United States | ~123% | Rising |

| France | ~112% | Rising |

| Spain | ~108% | Slowly falling |

| United Kingdom | ~101% | Rising |

| Canada | ~107% | Stable |

| Germany | ~64% | Falling |

| China (incl. local) | ~84% (official) — likely 110%+ | Rising |

| India | ~83% | Stable |

What 'debt crashing the economy' actually means

Debt does not destroy an economy by existing. It destroys an economy when bond buyers refuse to roll it over at any reasonable interest rate. The trigger is usually a loss of confidence in the issuer's ability to repay in real terms — through inflation, default, or capital controls. The damage cascades from there.

The three phases of a debt crash

Phase 1 — Bond market dislocation

Yields on long-dated government bonds rise sharply. The mechanism: buyers demand higher real returns to compensate for default and inflation risk. In 2022 the UK 30-year gilt yield doubled in four weeks during the Liz Truss mini-budget episode; pension funds were forced into emergency selling. The Bank of England had to step in. That was a foretaste, not a full crisis.

Phase 2 — Currency devaluation

If foreign investors lose faith, capital flows out and the currency falls. Imports become more expensive; inflation rises. The 1997 Asian crisis, the 2001 Argentine crisis, the 2018 Turkish crisis, the 2022 Sri Lankan default all followed this pattern. Each was a local crash; a global version is what most analysts now worry about.

Phase 3 — Inflation or deflation, depending on policy response

Central banks face a binary choice. (a) Allow rates to rise and trigger deep recession (1980 Volcker model — deflationary). (b) Print money to fund deficits and let inflation erode the debt (1923 Weimar, 1946 UK, modern Turkey and Argentina — inflationary). History shows democracies almost always choose inflation. Gold outperforms in both outcomes, but for different reasons.

Why gold outperforms in debt crashes — the mechanism

- No counterparty risk — physical gold is no one's liability and cannot default.

- No issuer — gold cannot be reprogrammed, frozen or inflated by any government.

- Real-value preservation — gold has tracked or exceeded inflation across every debt crisis since 1971.

- Universal acceptance — gold trades 24/7 in every major financial center.

- Central-bank validation — when governments themselves doubt fiat, they buy gold.

Historical case studies

1923 — Weimar Germany

The Reichsbank monetized war reparations debt. The Papiermark lost 99.99999% of its value in two years. Gold holders preserved purchasing power entirely. Bondholders lost everything.

1980s — Latin American debt crisis

Mexico, Brazil, Argentina and 14 other countries defaulted between 1982 and 1989. Local currencies collapsed; inflation hit triple digits. Gold, held by middle-class families in safety-deposit boxes, was the only asset that kept buying power.

2011–2012 — European sovereign debt crisis

Greek 10-year yields hit 35% in 2012. Greece, Cyprus, Ireland, Portugal and Spain all required bailouts. Gold rose to its then all-time high of $1,920/oz in September 2011 — the peak of the crisis.

2022–today — Sri Lanka, Pakistan, Egypt, Argentina

Multiple emerging-market sovereign defaults or near-defaults. In each, local gold prices reached record highs in local-currency terms while USD-gold was relatively flat. Households who held gold survived the currency collapse.

Could it happen to the US, Japan or Europe?

Major reserve-currency issuers (US, Eurozone, Japan, UK) cannot be forced into 'default' the same way emerging markets can — they print the currency their debt is denominated in. But that does not make them immune. The risk shifts from default to real-value default: debt is repaid in nominal terms but the currency loses purchasing power. This is the slow-motion default that has been happening since 1971 and is widely expected to continue.

The Japan paradox

Japan's debt-to-GDP is ~265% — far higher than any other major economy. Yet Japan has not had a sovereign-debt crisis. Why? Because ~92% of JGBs are held domestically (BoJ, pension funds, banks, households) and the BoJ owns over 50% of all outstanding JGBs. The model only works as long as domestic savers keep accepting low yields. The 2024 BoJ exit from yield-curve control was a first sign of strain.

Triggers to watch

- 1.Auction failures — a major Treasury or JGB auction with weak foreign demand.

- 2.Sovereign credit rating downgrades — US lost AAA from S&P in 2011, from Fitch in 2023, from Moody's in 2025.

- 3.Sharp DXY moves — currency stress signals reserve repositioning.

- 4.Central-bank gold buying acceleration — sophisticated capital flows.

- 5.MOVE Index spikes — bond-market volatility tends to precede equity volatility.

- 6.TED spread widening — interbank stress.

- 7.Credit-default swap blowouts on major sovereigns.

How to position for a debt crash

- 1.Diversify reserves — not all wealth in one fiat currency.

- 2.Hold 10–20% gold in physical, allocated and ETF form.

- 3.Avoid long-duration nominal bonds in inflation-driven scenarios.

- 4.Hold some short-duration sovereign debt for deflation-scenario optionality.

- 5.Maintain offshore brokerage access where legally permitted.

- 6.Know your jurisdiction's capital-control history — gold helps only if you can access it.

10% + (Sovereign debt-to-GDP × 0.05)A country with 200% debt-to-GDP would justify ~20% gold allocation under this heuristic. Illustrative only — not investment advice.

Why central banks already see the risk

Net central-bank gold buying has been positive every year since 2010 and hit record levels in 2022, 2023 and 2024 — over 1,000 tonnes per year. The buyers (China, Turkey, India, Poland, Saudi Arabia, Singapore) are not hedging against ordinary inflation. They are hedging against the failure of the dollar-Treasury reserve system itself.

Gold is money. Everything else is credit.

Frequently asked questions

How big is global debt right now?

About $315 trillion as of 2024, or 333% of world GDP — the highest in recorded history, per the Institute of International Finance.

Can the US really go bankrupt?

Not in a technical default sense — the US prints its own currency. But it can default in real terms by letting inflation erode the value of debt repayments. This is the historical pattern for reserve-currency issuers.

Why does gold go up in debt crises?

Because central banks usually monetize debt rather than allow default, money supply expands while gold supply does not. The supply mismatch shows up in price.

How much gold should I own if I worry about debt?

Mainstream guidance is 5–10% of net worth. Investors specifically positioning for a debt crisis often hold 15–25%, but this depends on local currency risk and tax treatment.

Will my bonds be worthless if the dollar crashes?

Not literally worthless — but long-dated nominal bonds can lose 30–50% of real purchasing power during periods of high inflation. Short-duration and inflation-linked bonds (TIPS) hold up better.

Is debt-to-GDP the only thing that matters?

No. Debt composition (foreign vs domestic holders, fixed vs floating rate, currency denomination) and the issuer's tax base matter as much. Japan has 265% debt-to-GDP and no crisis; Argentina has had crises at 50%.

Does Bitcoin work as a debt-crash hedge?

Track record is too short. Bitcoin has traded more like a risk asset than a hedge in the 2020 and 2022 sell-offs. Gold's 5,000-year track record is unmatched.

Disclaimer

Forecast and financial-advice disclaimer

This article discusses scenarios, history and macro principles only. It is not a forecast, financial advice or a recommendation to buy or sell any asset. Debt-crisis outcomes vary widely by jurisdiction. Consult a licensed advisor before acting.

Editorial disclaimer

Debt figures are from the IIF, IMF and central-bank disclosures, rounded to the latest reporting period. Live gold rates appear on the Goldify Quick Rates page.

Originality and AI policy

This article is human-written and edited by the Goldify editorial team. Every figure is reviewed against primary sources (IIF, IMF, BIS, IIF, central-bank publications). We do not publish AI-generated content unedited.